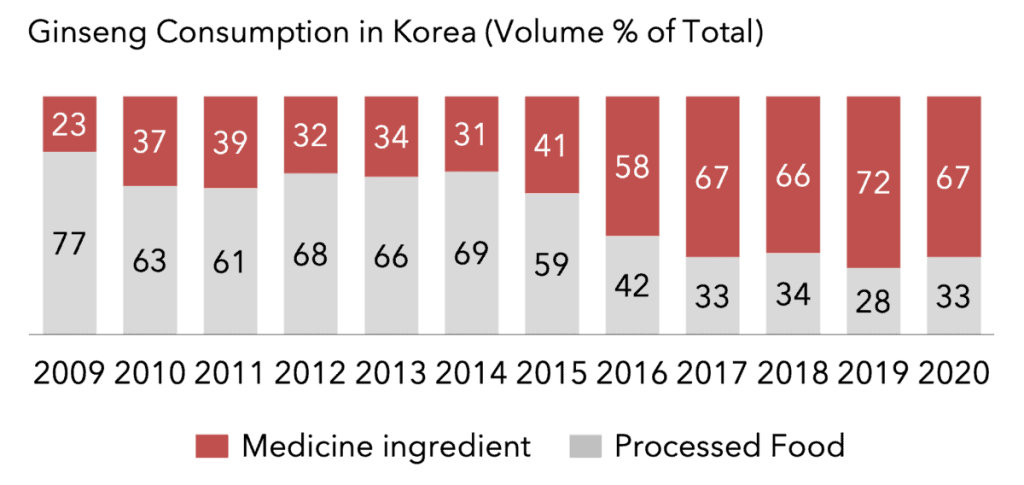

Ginseng is a Korean herbal supplement, that has traditionally been used as medicine but increasingly used as “health food” in recent years.

Please see below how ginseng changed from being used as mostly medicine to being consumed as food. (Source: Ministry of Agriculture, Food and Rural Affairs)

According to Korea Health Supplements Association, in 2021, ginseng accounted for close to one third of all health functional food in Korea.

(Source)https://www.khff.or.kr/

KGC’s brand is “Cheong Kwan Jang”. Its unique brand logo and identity, as shown below, is being copied by many competing brands in Korea.

Still, KT&G has over 70%-80% M/S thanks to KGC’s unmatchable brand built over the past 120 years, as well as product quality.

According to KT&G’s annual report (Mar 2022), KGC has a total of 265 patents.

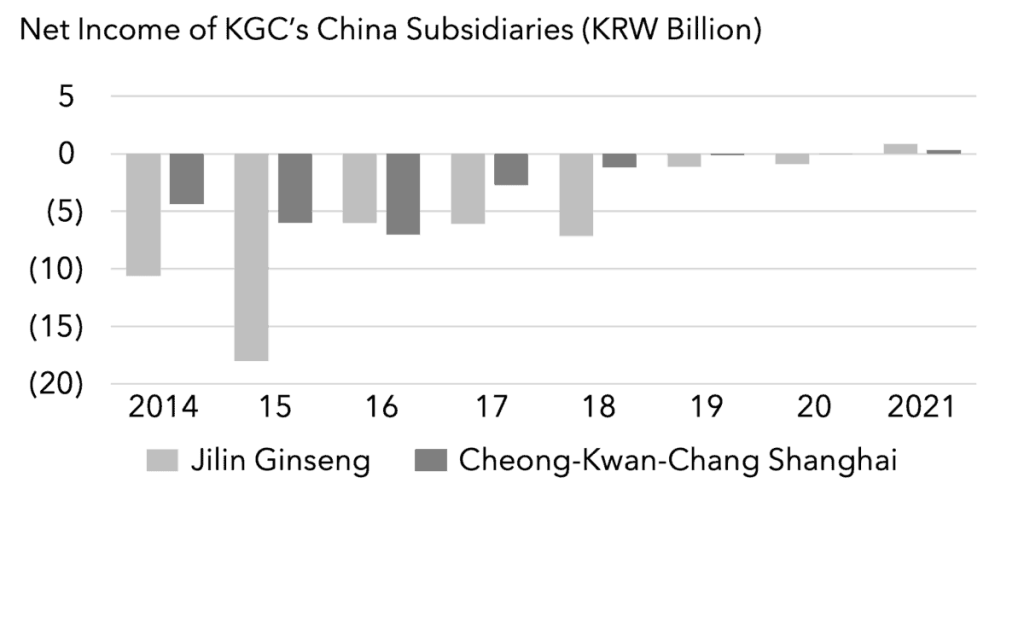

KT&G exports ginseng to China through two subsidiaries. Please see below the net income of these two companies. The companies only recently turned a profit.

Source: KT&G annual report